Prime Minister Narendra Modi keeps on lifting India in the global ranks.

Last week, the Indian economy jumped 23 spots in the World Bank’s 2018 Ease of Doing Business ranking. It occupies the 77th position, up from 100th in 2017.

And that comes on the top of another jump of 30 spots in the 2017 ranking from the previous year.

That’s remarkable progress. It sets India apart from other countries in the region — like Pakistan and Bangladesh, which ranked 136 and 176, respectively.

The Ease of Doing Business measures the impact of government regulations on starting and operating a business. Like the number of steps that are required to launch or to shut down a business, to deal with construction permits, or to obtain electricity.

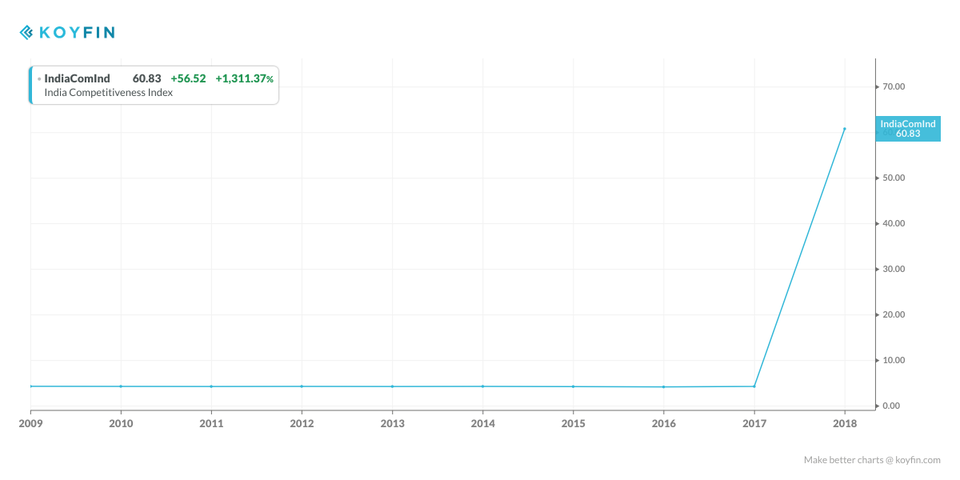

Meanwhile, the Indian economy has been rising in another global ranking, the World Economic Forum Report (WEFR) competitiveness report. That report ranks India 40th out of the 137 countries included, the highest it has ever been, up from 71st three years ago.

India Competitiveness Index

India Competitiveness Index

What’s behind India’s enormous rise in the Ease of Doing Business ranking?”

Three factors, according to Vijay Govindarajan Coxe, Distinguished Professor at the Tuck School of Business at Dartmouth.

“First, the BJP took power from Congress four years ago. BJP’s agenda is economic growth whereas Congress was all about populism,“ says Govindarajan. “The perception of India changed. Second, BJP relaxed rules and regulations and made it easier to do business. Third, now that China and the US have two formidable rival blocs, India has emerged as the largest economy for foreign companies seeking growth.”

LIU Professor Udayan Roy is skeptical about India’s frantic rise in global rankings. “Frankly, I am stunned,” says Roy. “I have no idea what actual policy changes — or improvements in implementation of existing policies — has led to this huge improvement. I hope India can at least maintain the rank in the years ahead. And, we’ll have to see if this translates into higher foreign investment. That’s what India needs.”

In fact, foreign investors have taken notice. India recorded a capital and financial account surplus of 17.43 USD Million in the second quarter of 2018, according to Tradingeconomics.com. That’s well above the average of 8.13 USD Million for the period 2010-2018. And a big factor behind the rally in Indian equities.

Meanwhile, improvement in the ease of doing business, the rise in competitiveness, and foreign capital flows have all helped place India among the world’s fourth fastest growing economies.

That’s according to the recently published IMF World Economic Outlook, which predicts that India’s economy will grow at 7.3% in 2018 and 7.4% in 2019, up from 6.7% in 2017, ahead of China’s.

Still, India’s rise in the world economy has yet to touch the masses. In fact, the average Indian is worse off under Modi.

That’s according to a Gallup survey last month, which finds that Indians’ ratings of their current lives nationwide are the worst in recent record, an average of4.0 on a 0-to-10 scale in 2017 – down from 4.4 back in 2014.

“Beginning in 2015, rural Indians began reporting increased difficulty paying for food,” says another Gallup report. “That year, more than one in four rural Indians (28%) reported not having enough money to pay for food at some point that year (compared with 18% of urban Indians who reported the same hardship)

And there are a few old villains that can eventually halt India’s gains in world rankings. Like the persistence of corruption, the rise of non-performing loans in state owned banks, and the fluid taxation system.

“India still has a long way to go. Hopefully, Prime Minister Modi will continue to accelerate the economic reforms,” adds Govindarajan.

Source: Forbes

Image Courtesy: Bloomberg

You may also like

-

World’s First-of-Its-Kind Fully Electric Double-Stack Freight Train from India: A World Benchmark

-

India’s Office Leasing Market Set for Strong FY27 as GCCs and Flex Workspaces Drive Demand

-

India Looks to Russia’s Tomtor Rare-Earth Deposit as Critical Mineral Race Intensifies

-

CSIR Transfers Seven Technologies to Industry, Releases Indian Reference Standards and Hands Quantum Sensing Components to DRDO

-

PM-VBRY: Centre Moves to Direct Incentive Stage in India’s Formal Jobs Push

{kind=link}